Company Owned Life Insurance and ESOPs

Life insurance is commonly used to fund buy-sell agreements in privately-held companies. Life insurance is often considered not only as a funding vehicle for buy-sell agreements but for ESOP repurchase obligation funding as well. The decision as to which entity is to own the insurance as well as how he insurance proceeds are to be used must be made carefully.

The advantages of having the corporation own the life insurance are significant:

- The corporation has unrestricted use of corporate-owned life insurance (“COLI”) cash values, including the funding of repurchase liability due to retirement or termination.

- Executive Strategy Whole Life is structured with significant cash value investment flexibility.

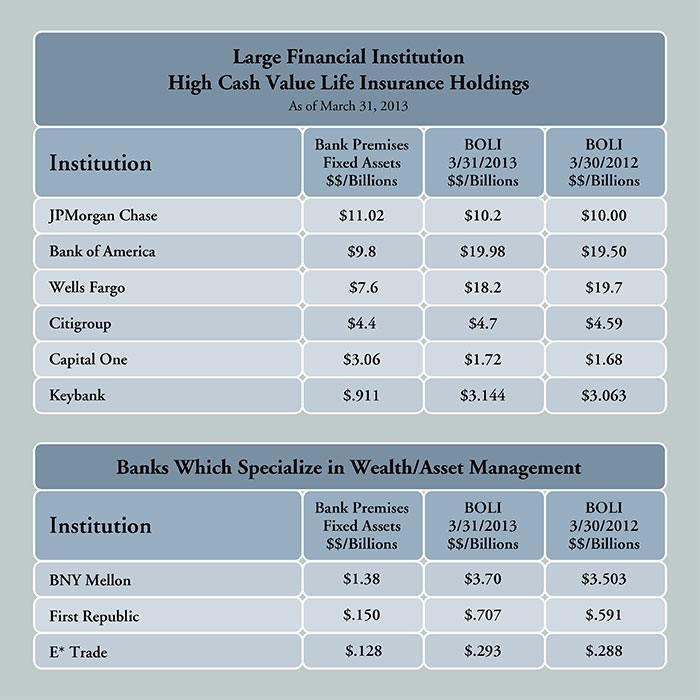

- The investment return of highly-rated life insurance companies exceeds other conservative investment options, i.e. money market accounts and certificates of deposit.

- Tax-free cash (subject to the Alternative Minimum Tax) received as death proceeds from the insurance policy by the corporation can be loaned to the ESOP or tax-deductible contributions can be made to the ESOP, enabling it to purchase the stock of the insured. If insurance proceeds are loaned to the ESOP, the company makes tax-deductible contributions to repay itself.

- Cash value of COLI grows on a tax deferred basis.

- A “waiver of premium option” for disability can be added to most policies.

In summary, maintaining the insurance with the corporation as owner, premium payer and beneficiary retains a great degree of flexibility for the corporation, maximizes the tax benefits of corporate-owned life insurance, and reduces fiduciary risk.

The income provided by a death benefit can be used by the corporation to directly purchase stock, or it can be contributed, or loaned to the ESOP.

The amount of insurance to have is a question that must be addressed separately by each ESOP company and will depend upon the projected account balances of plan participants, the level of “self-insurance” the corporation is willing to accept and the current and projected cash balance in the plan.